Discover how unified communications, voice-first AI, and real-time data integration help banks deliver seamless customer experiences while reducing cost and risk.

Banking customers expect instant, personalized service whether they call, chat, or walk into a physical branch. But if your contact center can’t see mobile app activity or your IVR provides a different balance than an agent, you’ve already lost trust. How you orchestrate conversations, data, and AI across communication channels directly impacts revenue, risk, and customer loyalty.

Get omnichannel wrong, and you’ll overspend on disconnected point solutions, miss out on AI-driven efficiencies, and trap customers in fragmented experiences. Get it right, and you’ll reduce cost-to-serve, accelerate product launches, and build a more agile platform for whatever comes next.

This guide covers omnichannel banking trends that drive real results, best practices for executing these strategies, and the foundational role of cloud communications and voice-first AI platforms in building unified, compliant, and scalable customer engagement.

Key takeaways

- Voice-first AI and conversational interfaces are becoming primary channels for high-value customer interactions

- Real-time data integration and event-driven architectures are essential for delivering consistent, context-aware banking experiences

- Cloud-native, API-first platforms help financial institutions consolidate fragmented communications stacks and embed artificial intelligence, data analytics, and compliance controls across the conversation lifecycle

What is omnichannel banking?

Omnichannel banking is a unified engagement strategy that delivers a continuous, context-aware experience across digital and physical touchpoints. It integrates backend systems and real-time data to ensure customer history and activity move seamlessly between channels.

An omnichannel banking model lets you:

- Recognize customers instantly, regardless of how they connect

- Retain context like last app sessions, pending transactions, and open service tickets across conversations

- Connect front-end interactions and back-office processes for faster, more accurate fulfillment

Why does it matter for enterprise IT and CX leaders?

Omnichannel banking directly impacts the outcomes that define success for enterprise IT and CX leaders: customer satisfaction, operational efficiency, risk management, and scalability.

The right approach delivers results like:

- Higher satisfaction and customer retention: The ability to move seamlessly between channels makes customers more likely to stay and recommend your services.

- Lower cost-to-serve: AI-powered containment and automation reduce high-touch interaction volume while improving resolution speed.

- Reduced error and rework: Unified real-time data helps eliminate the inconsistencies that erode trust and lead to repeat contacts.

- Faster product launches and partnerships: A centralized, API-first platform makes it easier to roll out new services or third-party integrations without rebuilding channel-specific workflows.

5 key omnichannel banking trends shaping the future of customer experience

Several trends are redefining the way the banking industry designs, delivers, and governs customer interactions. The most impactful approaches combine AI, real-time data, and automation with strong security and compliance controls.

Here are a few omnichannel banking strategies to keep on your radar and on your roadmap.

1. AI-powered personalization that spans every channel

Personalized experiences have evolved beyond basic cross-sell offers and marketing emails. Today, you must deliver context-aware, dynamic personalization across every service interaction.

AI and analytics now:

- Predict intent to surface likely reasons for contact before a customer reaches an agent or virtual assistant

- Tailor interaction flows, including interactive voice response (IVR) menus, chatbot conversations, and in-app help, based on customer behavior, product usage, and interaction history

- Deliver instant recommendations to agents, such as next best actions and compliant offers that match the customer’s risk profile

To capitalize on this trend, you must answer critical architectural questions: Where does real-time customer intelligence live? How do we govern it? How do we expose it consistently to both human agents and AI?

Omnichannel platforms that integrate with your core systems and analytics layers let you scale these personalized experiences without building dozens of custom connectors.

2. Voice-first and conversational AI as a primary interface

Even as digital self-service grows, voice remains critical for high-value interactions, like fraud alerts, disputes, complex lending, and wealth management. Integrating voice with conversational AI allows customer support to deliver smarter, faster outcomes.

Modernizing your voice strategy involves:

- Intelligent call routing that understands natural language, authenticates callers, and routes them to the right resource

- Virtual receptionists that resolve customer needs across voice and text, handing tasks off seamlessly if complexity or emotion escalates

- Real-time agent assist that listens to calls, surfaces relevant guidance and policies, and auto-generates summaries and dispositions

Consolidating fragmented telephony and IVR systems into a modern, programmable voice platform lets you scale AI capabilities while meeting strict compliance requirements.

3. Real-time data integration and event-driven experiences

Success in omnichannel banking requires data accuracy. When a mobile banking app displays one balance and an in-person agent provides another, you undermine your digital transformation efforts.

When AI doesn’t connect with your customer relationship management (CRM) platform, contact center, or core banking systems, these gaps become more apparent to customers. This problem affects about 52% of financial institution customers, according to a 2024 Capgemini report. It goes further to say that inconsistent messaging can make customers suspicious and less confident.

Maintaining consistent messaging requires:

- Event-driven architectures that publish meaningful changes (payments, logins, card swipes, disputes) as real-time events

- API-first integrations that connect contact center, unified communications (UC), CRM, and core banking systems to expose customer data consistently and securely

- Real-time journey orchestration that triggers personalized outreach like proactive alerts, dynamic routing, and targeted self-service the moment an event occurs

Omnichannel is a data and integration decision, not just an application choice. Your communications and contact center platform must function as a first-class citizen in your data ecosystem rather than sitting isolated at the edge.

4. Proactive and predictive engagement

Financial services customers expect institutions to spot issues before they escalate, whether that’s an upcoming overdraft, suspicious activity, or a stalled application. An Accenture study found that banks that focus on this level of “advocacy” grew 1.7 times faster than competitors.

To shift from reactive to proactive service, you need to:

- Trigger outreach across SMS, email, app notifications, and voice when behavioral signals or risk models demand action

- Route replies intelligently to self-service flows, bots, or live experts based on intent and customer value

- Measure and optimize complete journeys, not isolated touchpoints

Proactive service initiatives demand tight coordination between analytics teams, CX leaders, and IT. You need a platform that orchestrates outbound and inbound conversations seamlessly while enforcing controls for consent, preferences, and compliance.

5. Regulatory compliance automation and explainable AI

Regulators now scrutinize every AI-driven decision, disclosure, and data use in customer engagement. To mitigate risk, you must embed compliance controls directly into your omnichannel architecture.

A resilient compliance strategy requires:

- Automated capture and retention to record every interaction with tamper-proof audit trails that satisfy regulatory review

- Policy-driven access controls to define who accesses what data, for how long, and under what conditions

- Explainable AI models to document the logic behind decisions on credit and pricing to ensure fairness and consistency

Your platform choice carries direct risk. Choose vendors that standardize how you record, store, redact, and analyze conversations while integrating with your governance, risk, and compliance tools. Transparent AI models, clear data handling practices, and recognized certifications make audits faster and defenses stronger.

How are leading banks implementing omnichannel strategies?

Leading banks treat omnichannel as a multi-year transformation anchored around journey mapping, data unification, and platform consolidation. Several implementation patterns are emerging across large and mid-market financial institutions.

Start with high-impact journeys, not channels

Successful teams don’t try to fix everything at once. Instead, they pick three to five priority journeys and work backward.

This process involves:

- Mapping the current experience across all channels, including in-branch and back-office handoffs

- Quantifying pain points like abandonment rates, repeat contacts, manual work, and compliance risk

- Designing a target flow that blends self-service, proactive outreach, and expert support

- Identifying the platform capabilities and integrations you need to deliver that flow

A journey-led approach delivers two critical outcomes: more surgical technology investments and a stronger business case for stakeholders focused on customer outcomes.

Consolidate communications and contact center platforms

Fragmented telephony, private branch exchange (PBX), and contact center environments split by line of business or region make it nearly impossible to deliver consistent omnichannel experiences or deploy AI at scale.

Modernizing this infrastructure requires moving to cloud-based communications and contact center platforms that:

- Unify enterprise communications by bringing voice, video, messaging, and contact center onto a single foundation

- Centralize routing and reporting to provide a native, omnichannel view across every customer interaction

- Enable programmable integration through open APIs and real-time event streams to push context and trigger actions between your communications platform and core systems

Consolidating your stack reduces technical debt and creates the architectural foundation required for advancements in AI-driven customer intelligence.

Invest in change management and frontline adoption

Customer-centric omnichannel banking changes how your agents, bankers, and specialists work every day, not just what technology they use. Success depends on preparing your workforce for a cross-channel environment.

This transformation requires:

- Training agents and branch teams on new tools, scripts, and processes that support seamless journeys

- Giving supervisors real-time visibility into queues and performance across channels so they can coach effectively and adjust staffing

- Involving compliance, risk, and legal teams early in design to eliminate rework and last-minute blockers

To drive stronger adoption and deliver more durable results, treat communications and contact center modernization as a people and process transformation, not just an IT project.

Challenges and risks of omnichannel banking

The benefits of omnichannel banking are clear, but the risks are equally significant. Integrating legacy systems, new channels, and AI while maintaining strict reliability and compliance creates recurring challenges.

Integration complexity and technical debt

Legacy cores, aging telephony, multiple CRMs, and line-of-business point solutions create integration nightmares.

Without a clear strategy, you face:

- Duplicate integrations between each channel and each system of record

- Inconsistent data models that break personalization and reporting efforts

- Fragile point-to-point connections that block your ability to change or scale

Smart banks reduce this risk by standardizing on strategic platforms that provide unified communications and contact center capabilities with built-in governance.

Vendor lock-in and loss of flexibility

The shift to cloud-based platforms can create vendor dependency if you choose the wrong partner. Without the right safeguards, switching providers or adding capabilities becomes costly and disruptive.

Protect your flexibility by choosing vendors that offer:

- Open APIs and documented data export so you control your data and integrations

- Configurable workflows instead of custom code that locks you into a single platform

- Contract terms that support phased rollouts and clear exit paths

Partners who embrace interoperability and industry standards give you a stronger negotiating position and more long-term agility.

Scalability, performance, and reliability

When you consolidate interactions onto fewer platforms, you concentrate risk. A single outage can affect voice, chat, and digital channels simultaneously, making uptime, latency, and call quality non-negotiable.

Evaluate platforms on operational reality, not marketing promises:

- Review uptime history and real-time status transparency through documented performance data

- Examine network architecture for redundancy layers, carrier diversity, and traffic management capabilities

- Test real-world performance in your geographies and use cases before you commit

Enterprise-grade providers build global carrier connectivity, continuous monitoring, and proactive incident response directly into their infrastructure.

Data security, compliance, and privacy concerns

Every interaction in omnichannel banking carries account details, personally identifiable information (PII), and sensitive data. It’s essential to build security and compliance into your communications stack from day one rather than bolting them on later.

Focus on four critical areas:

- Data protection and encryption that secure data in transit and at rest using industry-standard protocols, strong key management, and role-based access controls

- Recording, retention, and auditability to capture interactions securely and provide tamper-proof audit trails that satisfy regulators and internal investigations

- Data residency and sovereignty to meet regional requirements for where you store and process data when operating across borders

- Privacy and consent management to track and honor customer preferences for recording, outreach, and data usage consistently across every channel

Vetting how vendors secure their own infrastructure, including certifications, incident response protocols, and data generated by AI features like transcription and summarization, is a critical final step.

By addressing the above concerns early through smart architecture, careful vendor selection, and clear policies, you can unlock omnichannel banking’s benefits without exposing your institution to avoidable risk.

Strategic priorities for navigating omnichannel banking transformation

Omnichannel banking trends can feel overwhelming when you’re juggling regulatory change, modernization pressures, and budget scrutiny. Defining a small set of strategic priorities is a good way to guide your technology and investment decisions.

Anchor everything in customer journeys and measurable outcomes

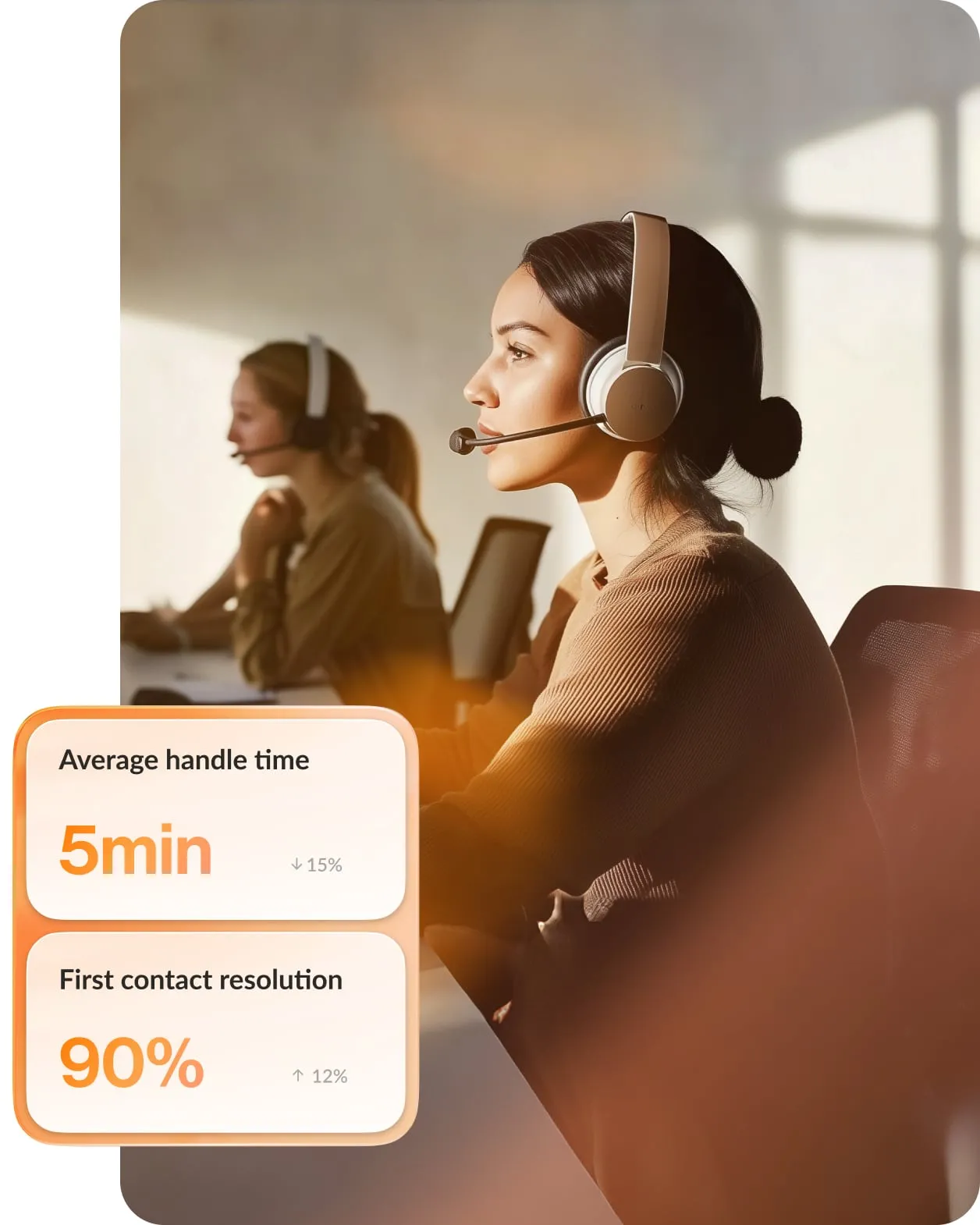

Align with business and CX leaders on a handful of priority journeys and metrics, such as containment rates, first-contact resolution, and time-to-fulfill.

Use these to:

- Prioritize channels and segments to determine which use cases you tackle first

- Evaluate vendors on their ability to move those specific metrics

- Build iterative roadmaps that let you test, learn, and scale

Anchoring decisions in journeys and outcomes allows you to defend investments more effectively and pivot faster when conditions change.

Treat data and integration as first-class design concerns

Personalized experiences, proactive outreach, and AI coaching only work when data flows cleanly between systems.

Create your roadmap using three integration priorities:

- Standardizing data models for customers and interactions across every channel and system of record

- Defining reference architectures that connect your communications platform to core banking, CRM, analytics, and risk systems

- Investing in API management, event streaming, and integration governance to avoid recreating point-to-point problems in the cloud

When you design omnichannel as part of your broader data strategy, you build durable experiences.

Operationalize AI responsibly across the conversation lifecycle

AI drives your omnichannel strategy, but you should still treat it as an operational capability instead of a one-time experiment.

Build confidence and control by:

- Starting with low-risk, high-value use cases like call summarization and real-time agent assist that deliver immediate wins

- Setting clear guardrails and human oversight for AI decisions in regulated areas like credit, pricing, and dispute resolution

- Measuring AI performance continuously and feeding insights back into model tuning and process refinement

Platforms that embed AI across routing, self-service, and analytics accelerate deployment while maintaining consistent controls and full visibility into every interaction.

Invest in governance, change management, and cross-functional alignment

Omnichannel banking spans IT, operations, branches, marketing, risk, compliance, and HR. Build clear governance structures and change management plans to keep teams aligned and momentum sustainable.

That means:

- Establishing a cross-functional steering group with real decision-making authority

- Defining design standards and reusable patterns for journeys, channels, and AI use cases

- Creating feedback loops that connect frontline staff and customers directly to product and technology teams

Strong cross-functional governance lets you move faster with more confidence and make smarter bets on which omnichannel banking trends will deliver the most value.

Build a smarter omnichannel foundation

Omnichannel banking is an ongoing transformation that touches every part of how you serve customers and manage risk. The trends covered above are essential for staying competitive and meeting customer expectations in 2026 and beyond.

Start with journeys, not channels. Pick three high-impact customer experiences, map where fragmentation costs you the most, and design backward from there. Then audit your communications stack. If you’re running separate systems for telephony, contact center, and UC, you’re paying a hidden tax in complexity, cost, and missed AI opportunities. Consolidation creates the foundation for everything else.

If you’re ready to simplify your architecture and accelerate your omnichannel vision, explore how a unified, cloud-native platform can help. Learn how RingCentral supports omnichannel customer experiences in banking to benchmark your own strategy and build a more agile, AI-ready foundation for the years ahead.

Originally published Mar 04, 2026